The Oil and Gas Accumulator Market plays a crucial role in ensuring operational safety, energy efficiency, and pressure management across hydraulic systems used in oil and gas exploration, production, and processing. Accumulators are specialized energy‑storage devices that store potential energy as pressurized fluid, deploying it instantly during peak demand, surge events, or critical operational moments — such as in blow‑out preventers (BOPs), drilling rigs, and offshore platforms.

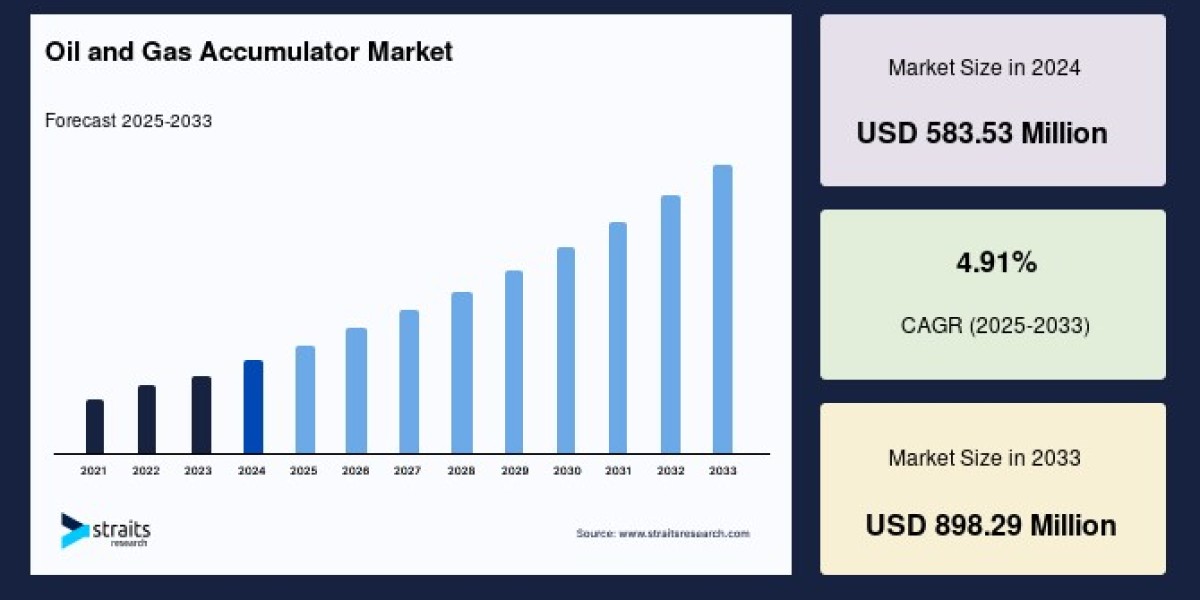

Recent market analyses indicate that the industry was valued at approximately USD 1.66–1.7 billion in 2024‑2025 and is projected to grow to around USD 2.6 billion by 2035, registering a compound annual growth rate (CAGR) of around 4.1–4.2% over the forecast period.

This steady growth reflects increasing energy demand, expansion of oil & gas exploration activities, more stringent safety standards, and technological innovation in accumulator designs — from traditional hydraulic units to smart, digitally optimized systems.

Download Your Sample Report Now@ https://straitsresearch.com/report/oil-and-gas-accumulator-market/request-sample

Market Overview

The oil and gas industry depends on reliable hydraulic systems for fluid handling, pressure regulation, energy recovery, shock absorption, and pressure stabilization. Accumulators, such as bladder, diaphragm, and piston types, serve these functions across upstream, midstream, and downstream operations.

Bladder accumulators continue to dominate due to their reliability and adaptability in critical applications such as pipeline pressure control and BOP systems.

Diaphragm and piston accumulators offer advantages in specific scenarios where precise control, high pressure, or variable performance is required.

Regional demand varies, with North America holding the largest market share due to extensive shale and offshore drilling activity. The Asia‑Pacific region, particularly China and India, is also emerging as a major growth contributor, driven by rising energy needs and infrastructure development.

Market Restraints

Despite positive growth trends, the market faces several constraints:

High Initial Capital Costs:

Accumulators involve significant upfront investment and substantial logistical costs due to their size and weight. This can slow adoption, especially in smaller operations or regions with limited capital availability.Environmental and Regulatory Pressures:

Strict environmental regulations, particularly around drilling safety and emissions, can increase compliance costs for hydraulic system deployment.Volatility in Oil Prices and Energy Transition:

Fluctuating oil prices and the global shift toward greener energy alternatives may reduce investment in traditional oil & gas equipment, impacting accumulator demand in certain sectors.

Market Opportunities

Despite restraints, several growth opportunities are emerging:

1. Digital Transformation and Smart Accumulators

With increasing adoption of digital technologies, sensors, and predictive maintenance systems, accumulator performance and reliability are improving dramatically. The integration of IoT and advanced monitoring allows operators to optimize maintenance, reduce downtime, and enhance overall system efficiency.

2. Expanding Offshore Drilling and Onshore Exploration

The continued search for new hydrocarbon reserves and higher offshore activity opens opportunities for accumulator manufacturers, particularly in safety critical systems such as BOP controls.

3. Energy Storage and Efficiency Trends

Accumulators contribute to energy recovery and storage in hydraulic systems, aligning well with industry efforts toward energy efficiency and reduced operational costs.

Available for purchase with detailed segment data, forecasts, and regional insights. Buy Now@ https://straitsresearch.com/buy-now/oil-and-gas-accumulator-market

Market Segmentation

The oil and gas accumulator market is broadly segmented as follows:

1. By Type

Bladder Accumulators

Diaphragm Accumulators

Piston Accumulators

Each type serves different operational needs, with bladder units leading due to versatility and reliability.

2. By Application

Offshore applications

Onshore fields

Blow‑out preventer (BOP) systems

BOP-related applications are significant due to safety and rapid response requirements.

3. By Region

North America

Europe

Asia‑Pacific

Latin America

Middle East & Africa

North America and Asia‑Pacific are key growth regions.

Key Players and Revenue Insights

The market is moderately fragmented, with a mix of global hydraulic specialists and energy equipment providers:

Major Players Include:

Parker Hannifin Corporation – Leading hydraulic systems provider; reported ~USD 19.9 billion in total sales (latest fiscal, reflecting broader hydraulics revenue).

Schlumberger Ltd. – Major oilfield services firm integrating accumulator solutions within digital and subsea offerings.

Halliburton Company – Advanced accumulator technologies and digital platforms for offshore operations.

TechnipFMC plc – Co‑developing digital subsea systems with standardized accumulator modules.

Eaton Corporation, Bosch Rexroth AG, Flowserve Corporation, Weatherford International, and Aker Solutions.

While specific accumulator revenues aren’t always publicly separated, these companies’ broader hydraulic and energy equipment revenue reflects their market strength.

Latest Developments and Collaborations

Recent industry developments showcase innovation and partnership trends:

TechnipFMC and Kongsberg Gruppen announced a strategic partnership (March 2025) to develop next‑generation subsea control systems with standardized hydraulic accumulators.

Flowserve Corporation secured a major supply contract with Shell (Dec 2024) for high‑flow hydraulic accumulators for offshore platforms.

Emerson Electric launched new high‑capacity, corrosion‑resistant hydraulic accumulators (July 2024).

Such collaborations highlight the shift toward digital, high‑performance solutions tailored for modern energy challenges.

Frequently Asked Questions (FAQs)

Q1. What is the size of the oil and gas accumulator market?

The market was valued at approximately USD 1.66–1.7 billion in 2024–2025 and is projected to reach around USD 2.6 billion by 2035.

Q2. What is driving market growth?

Growth is driven by increasing energy demand, safety requirements in drilling operations, and technological advancements such as digital monitoring.

Q3. Which accumulator type leads the market?

Bladder accumulators lead due to durability, reliability, and wide application in critical systems.

Q4. Who are the key market players?

Key players include Parker Hannifin, Schlumberger, Halliburton, TechnipFMC, Eaton, Bosch Rexroth, and Flowserve.

Q5. What challenges does the market face?

High initial costs, regulatory pressures, and volatile oil prices are key restraints.

Conclusion

The Oil and Gas Accumulator Market is poised for steady growth over the next decade, underpinned by expanding drilling activities, safety and efficiency needs, and digital innovation. While high costs and environmental concerns pose challenges, advances in smart hydraulic systems and collaboration among key industrial players offer substantial opportunities. With ongoing investments in offshore technologies and energy storage applications, the sector is expected to remain integral to oil & gas operations worldwide.

About Us

Straits Research is a market intelligence company providing global business information reports and services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insight for thousands of decision-makers. Straits Research Pvt. Ltd. provides actionable market research data, especially designed and presented for decision making and ROI.